I Already Have a Mediclaim, Why Should I Buy a Corona Kavach Policy?

Corona Kavach – Health Insurance Policy for COVID-19

“If you had Corona Kavach policy, you would have saved the entire medical bill of Rs 2 lakhs”, these words rang in Raj’s ears as he walked away from the hospital counter. Raj recently started his first job in a reputed MNC and had prudently saved his salary in the lockdown months as he worked from home. Little did he expect that his father will get tested positive with Covid-19 virus so soon. Had he purchased an Online Corona Kavach Policy, he would have easily gotten the benefits.

Nations around the world are struggling to fight Corona or COVID-19 pandemic, which has already affected more than 2.7 crore people worldwide and taken a toll of more than 8 lakh plus human lives (as we write this article). The magnitude of the spread and the repercussions of this disease is indeed unprecedented in recent human history. The sky-high costs of COVID treatment have spurred a conversation around the rising costs of healthcare in India. Once a person is infected, you will burn a hole in your pocket on hospitalization expenses like room rent, ventilators, oxygen masks, medicines, and meals. And to add to this, there are pre and post-hospitalization expenses that include diagnostic tests, medicines, consultation charges, ambulance charges, and the like. With no vaccines available yet, hospital bills run into lakhs of rupees.

This pandemic outbreak has indeed been an eye-opener for people who are not insured medically. Are you also worried about financial stress when you step out of the home to work? Or for taking care of your loved ones in a good facility? Worry not!

You can buy additional health insurance cover specially catering to Covid-19 patients, and that too at a very affordable cost. All insurers have now released Corona Kavach policies according to IRDAI guidelines. It provides much-needed financial security and peace of mind to its subscribers. It covers all the costs related to Covid-19 treatment even after hospital discharge.

What is a Corona Kavach Policy?

Corona Kavach policies are indemnity-based policies, which means that it will reimburse you for expenses incurred by you after you are tested positive, it does not give you a guaranteed benefit amount as in the Corona Rakshak policies. It provides a shorter waiting period than general health insurance policies to ensure that new subscribers can get the maximum benefit. You can buy corona kavach policy online for yourself or for the whole family as a floater.

I Already Have a Mediclaim Why Buy a Corona Kavach Policy?

Although most mediclaim policies have included Corona treatment in the cover, there are some insurers who may not settle a claim if a disease is declared a pandemic or an epidemic. You need to read the policy document carefully or clarify with your insurer to understand if you have a cover.

There are several other advantages of buying a Corona Kavach Online Policy:

- Your mediclaim policy does not cover the cost of consumables like PPE kits, goggles, footwear, sanitisers, and disinfectants, which are additionally required in Covid-19 treatment.

- You have to pay the premium one time, as it is a short-term policy.

- If home quarantine is recommended by a healthcare professional instead of hospitalization, the costs for that will also be covered.

- Your mediclaim shall remain unaffected and you can still avail of the benefit of a no-claim bonus (if applicable).

What are the main features of a Corona Kavach Policy?

Because of IRDAI guidelines, most policies have similar conditions.

- Any person between the ages of 18-65 can purchase this policy for themselves or as a floater for their family. Dependent children can also be covered.

- They have a waiting period of 15 days, which means the expenses incurred during this period will not be covered.

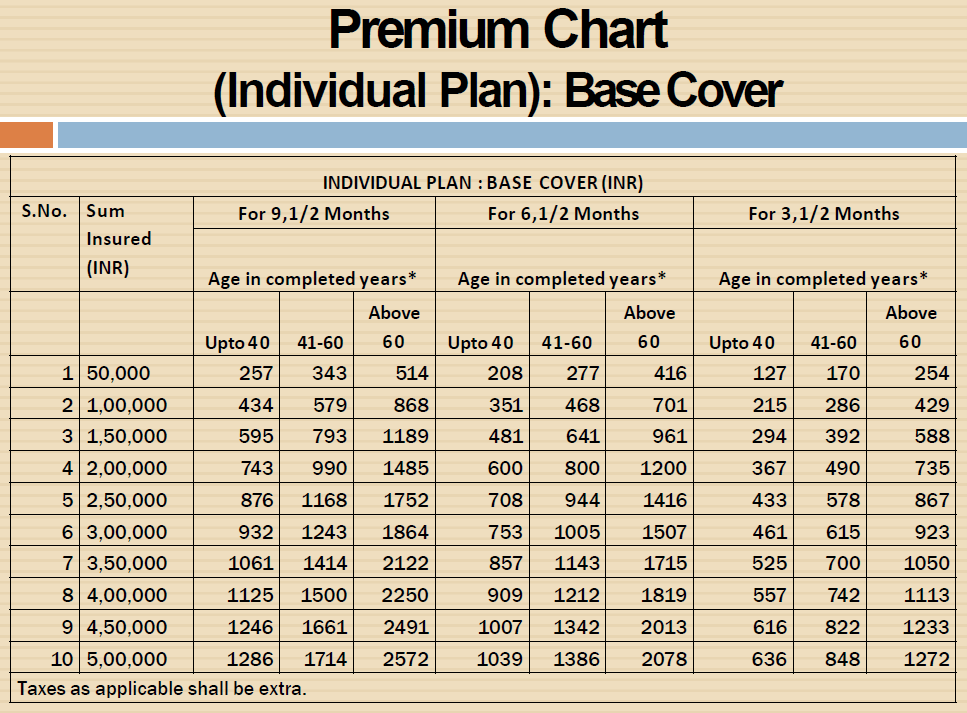

- The base sum insured ranges between Rs 50,000 and Rs 5,00,000 in increments of Rs 50,000.

- They cover expenses incurred for hospitalization when hospitalized for 24 continuous hours. They also cover co-morbidity (or other diseases) arising out of the treatment of Covid-19.

- They cover medical expenses incurred towards in-home care treatment, Ayurveda, Naturopathy, Unani, Siddha, and homoeopathy also. For home care treatment, it must be advised by a medical professional and there should be a record of an active line of treatment.

- They also cover expenses incurred within 15 days of pre-hospitalisation and 30 days post-hospitalization.

- The insured can also avail of an optional hospital daily cash cover in which the insurer will pay up to 0.5% of the sum insured for every day of hospitalization for up to 15 days.

- Policy periods can be chosen from three and a half months (105 days), six and a half months (195 days), and nine and a half months (285 days).

- Offers a 5% discount to health professionals like doctors, nurses, and a 10% discount to rural and online registrations.

Now the main wordings are the same across the industry but there is a notable difference in the premium requested by different insurers. Let us compare two policies:

Type 1 – Corona Kavach Policy:

Below is an indicative table of premiums for one policyholder. The detailed schedule for the family floater option can be seen here

Type 2 – Corona Kavach Policy:

Below is an indicative table of premiums for one policyholder. The detailed schedule along with floater options can be seen here

To sum it up

So words from the wise – it’s always better to be safe than sorry. Having a Covid-19 policy can indeed provide financial relief to the victim and his family who are already under emotional stress. In the current times when the situation is worsening and the cases are rising exponentially every day, it is better to be insured against Covid-19 exclusively by buying a separate policy, leaving your medical insurance untouched.

However, when you come down to choosing the right Corona Kavach Policy, know this – while all Corona policies have similar wordings due to IRDAI regulation, the major difference lies in the premium calculation. In general, private sector companies are charging higher premiums than PSU companies as we have seen above.

In fact, in the current scenario, it makes all the sense for a corporate to get its employees insured under Corona Kavach for the safety and security of the corporate and its employees. If you do have not any corona kavach policy buy online to know more click here – https://bit.ly/45KXmEe or Call +91- 9109910688, 7869955851

{kind=link}