Juniper Hotels IPO: Should You Check In or Check Out? A Deep Dive Analysis

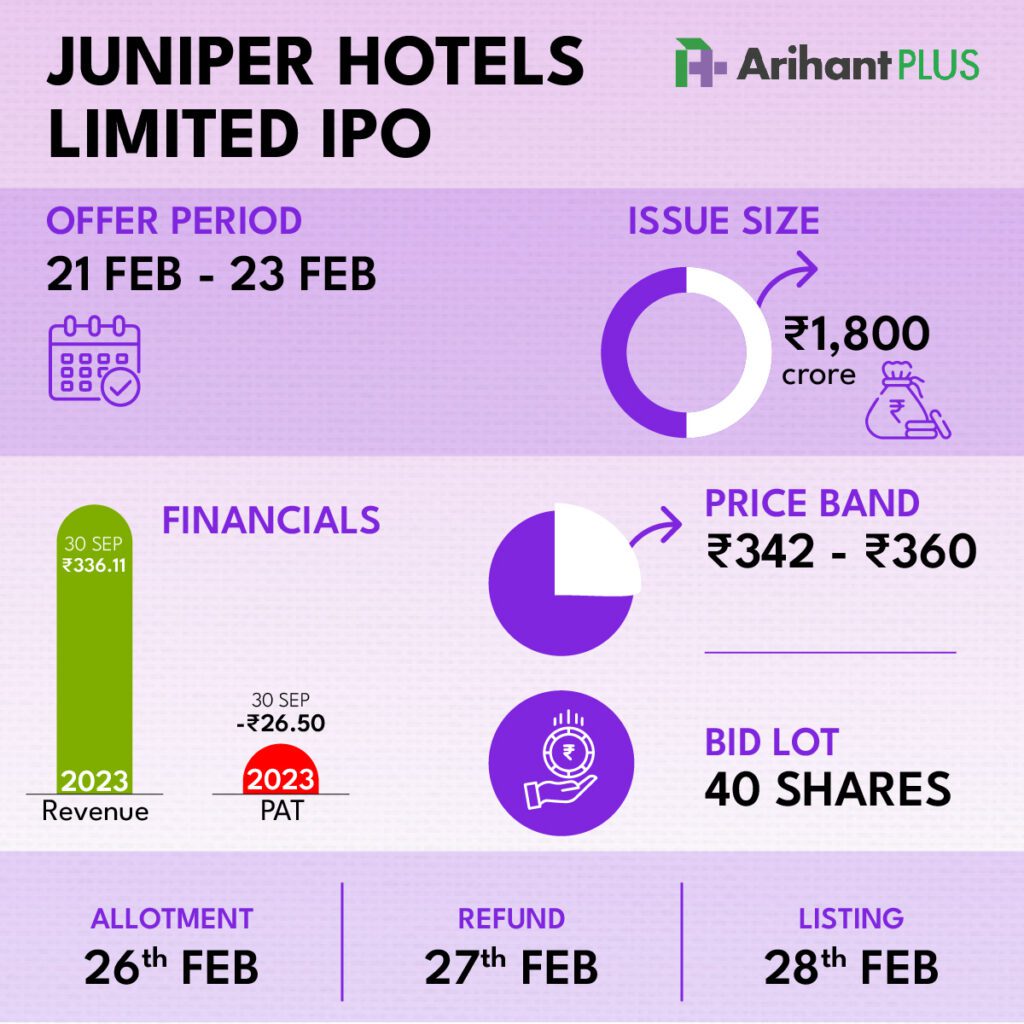

Juniper Hotels Limited, the king of Hyatt-affiliated hotels in India, is finally going public with its first initial public offering (IPO) on Wednesday, 21st February 2024, with the bidding period closing on 23rd February. The company is planning to raise ₹1,800 through the IPO. Minimum investment has been earmarked to ₹14,400 (40 shares).

Is this an investment opportunity you shouldn’t miss, or are there hidden red flags lurking in the plush lobbies? We dive deep into the company’s strengths, weaknesses, and future prospects to help you decide.

Company Overview

Juniper Hotels is a collaboration between Indian powerhouse Saraf Hotels and global giant Hyatt, Juniper Hotels brings exceptional hospitality to seven key cities from vibrant Bengaluru to majestic Agra. Established in 1985, today Juniper is a leading player in the Indian luxury hotel market. This unique joint venture boasts strong ownership: Saraf Hotels leverages local expertise, Hyatt brings global reach, and Juniper Investments strengthens the local connection.

As of 30th September 2023, Juniper Hotels owns and operates a portfolio of seven hotels and serviced apartments, totaling 1,836 rooms across various categories. These properties are strategically located in key Indian cities like Mumbai, Delhi, Ahmedabad, Lucknow, Raipur, and Hampi. Juniper Hotels is poised for expansion and continued success in India’s booming hospitality sector.

IPO Objective

Juniper Hotels IPO is a fresh issue, intending to raise ₹1,800 crore through fresh equity, offering investors direct participation in the company’s growth with no existing shareholders selling their holdings. The majority of the proceeds, ₹1,500 crore, will be used to pay off debt held by both Juniper and its subsidiaries, improving their financial health and flexibility. The remaining funds will be directed toward strategic initiatives and overall business growth.

IPO fine print and listing details

CLSA India, JM Financial, and ICICI Securities are the book-running lead managers of the Juniper Hotels IPO, while Kfin Technologies Ltd is the registrar for the issue. The shares of the company will be listed on both BSE and NSE. Wednesday, February 28 is the tentative date of listing.

The company has reserved

- 75 percent of the offer to qualified institutional bidders (QIBs),

- 15 percent for non-institutional investors (HNI), and

- 10 percent allocated to retail investors.

A brand-name beauty

With a portfolio boasting seven hotels and serviced apartments across key cities like Mumbai, Delhi, and Ahmedabad, Juniper Hotels holds the crown for owning the most “Hyatt” establishments in India. This translates to instant brand recognition and access to Hyatt’s global network, a powerful advantage in the hospitality industry.

More than just a pretty face

Juniper Hotels doesn’t rely solely on its brand association. They boast a keen eye for strategic site selection, choosing locations with high potential for both business and leisure travelers. Their diverse portfolio caters to different segments, ranging from luxury havens like the Grand Hyatt Mumbai to upscale serviced apartments like Citrus Serviced Apartments, ensuring a broader customer base.

On the financial front, the company’s revenue quadrupled in the past three years, thanks to a rebound in the number of guests and the prices of rooms after the COVID-19 crisis. In addition, it reduced its loss to ₹1 crore in FY23 from ₹199 crore in FY21, which is a positive sign. The boom in the travel and tourism industry post Covid-19 has benefitted Juniper Hotels and it seems this trend is here to stay.

A partnership built to last

Their 40-year-long partnership with Hyatt isn’t just a number; it’s a testament to their strong relationship and shared vision. This collaboration gives them access to Hyatt’s operational expertise, marketing muscle, and industry insights, propelling them ahead of the competition.

Numbers telling a story

Juniper Hotels has witnessed an impressive growth trajectory, with its revenue soaring from ₹166.35 crores in FY21 to a whopping ₹666.85 crores in FY23. This translates to a near-quadruple increase in just two years, showcasing their ability to capitalize on market opportunities.

Potential threats to Juniper Hotels

But wait, there’s more. While the headlines might scream success, a closer look reveals some potential hiccups.

The financials and debt raises red flags

The three-year average return on equity (ROE) and return on capital employed (ROCE) of Juniper Hotels are -24.4% and 1.8%, respectively. Moreover, the company has not been profitable in the last three financial years. Besides, Juniper Hotels carries a sizeable debt burden of ₹2,252.75 crores as of September 2023. This hefty debt limits their financial flexibility and can hinder their ability to invest in future growth or manage operational costs effectively.

Putting all your eggs in one basket

A significant portion of their revenue, that’s a whopping 90.48%, comes from just three hotels in Mumbai and Delhi. This high concentration risk means that any economic downturn or change in consumer preferences in these regions could significantly impact their business performance.

Fixed costs can be fixed expenses

Operational expenses like employee salaries and lease rentals don’t fluctuate with occupancy rates. This means even during low seasons, they have high fixed costs to bear, potentially impacting their profitability.

Hyatt’s grip on the keys

Their reliance on Hyatt for hotel operations and brand usage comes with its own set of risks. Any changes or non-renewal of these agreements could have a negative impact on their business and finances.

A recent acquisition raises eyebrows

Their recent acquisition of CHPL and CHHPL in September 2023 could pose potential risks, including write-offs or losses from subsidiary operations, further affecting their financial health.

So, should you invest?

The decision ultimately lies with you. While Juniper Hotels has a strong brand, strategic approach, and impressive growth potential, the debt burden, concentration risk, operational challenges, and reliance on Hyatt cannot be ignored. However, since the primary objective of the IPO is to repay outstanding debt to the tune of ₹1,500 crores. With the debt reduction, the interest burden on the company will ease and it will be well-positioned for growth.

With tourism on the rise, Juniper Hotels could be a good investment opportunity for high-risk investors and they can consider Subscribing to the issue.

Take a look at the key points below

| Feature | Pros | Cons |

| Brand & Portfolio | Largest “Hyatt” owner in India, Diverse portfolio across segments | Brand reliance, Limited presence outside major cities |

| Partnership | 40-year partnership with Hyatt, Access to expertise and network | Dependency on Hyatt for operations and brand |

| Financials | Strong revenue growth, Expanding footprint | High debt burden, Recent acquisition risks |

| Operational Efficiency | Focus on optimization and diversification | High fixed costs, Concentration risk |

Our verdict

At the upper band of ₹360, the issue is valued at an EV/EBITDA of 25.6x based on FY23 EBITDA. While we recommend “Subscribe” based on the company’s strengths and strategic initiatives, we urge you to carefully consider the risks mentioned above before making your investment decision.

{kind=link}