Should I invest in LIC IPO?

In this article

Do you remember the insurance uncle? The sweet, middle-aged man, who was often seen talking with your parents. He was your parent’s friend, advisor and confidant.

This agent or “insurance uncle” is a figure many of us grew up to know as the face of LIC. What we didn’t know was that he was a part of a gigantic distribution network that spawned the length and the breadth of the country.

In a country with 138 crore people, this 65 year old behemoth issues 3 out of every 4 new insurance policies. Such is the extent of its influence over an Indian consumer’s mind “insurance” in India means LIC.

Let us see what makes this brand synonymous with the entire industry.

The Fundamentals

Insurance is a business of trust and to ensure that insurers are able to pay their customers when required, it is highly regulated by IRDAI.

The customers pay premium amounts to LIC. LIC collects all these premia (which form its Assets Under Management) and invests them in various stock market and money market instruments, in order to generate returns. When an insured customer makes a claim, or a policy completes its term they get the payment which was decided in the policy.

LIC makes money on its investments, the customer makes money and gets a safety net. Now that’s a win-win!

The Volume

LIC is the 5th largest player globally in terms of premium and the 10th largest in terms of total assets.

With an AUM of more than 39 lakh crores* LIC’s pockets are bigger than the GDP of several economies. It is the biggest asset manager in the country, with an AUM of 3.3 times the AUM of all its competitors combined. In fact, LIC’s AUM is more than the AUM of the entire mutual fund industry in India. The behemoth owns 4% of the total market capitalization of the NSE. Through all its investments, it earns more than ₹1.5 lakh crore every year by means of dividends.

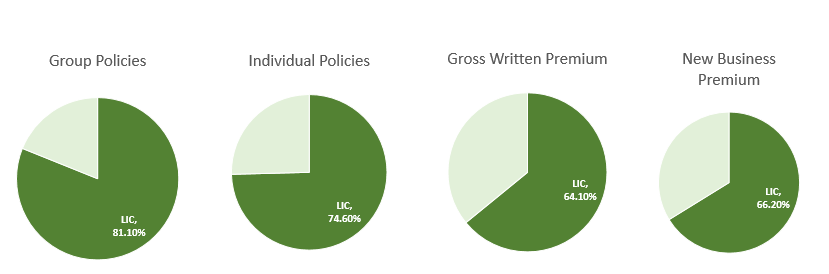

Market Share

One look at the insurance industry, and you know that LIC captures the lion’s share of the market, beating all its competitors by a mile.

Distribution

It markets all types of investment avenues – ULIP, saving insurance, term insurance, health insurance, annuity and pension products with its huge network of 1.35 million insurance agents. These agents give private insurance agents a run for their money with their 3x productivity. Their network of 8 main offices, 2048 branches, 113 divisional offices and 1,554 satellite offices in India, helps them cater to each nook and cranny of the country.

LIC’s omnichannel distribution platform comprises individual agents, bancassurance partners, alternate channels- corporate agents, brokers and insurance marketing firms, digital sales, micro insurance agents, and point of sales persons.

Looking Forward

The Indian insurance industry (measured by growth in premium) is growing at a five-year CAGR of 11% and is expected to grow at 14-15% CAGR over the next 5 years. It is expected to reach a whopping ₹12 trillion!

India’s life insurance penetration stood at 3.2% in CY20 vs the global average of 3.3%. India also has a penetration gap of 83% in CY19 which is higher than all Asia- Pacific countries. This shows the growth potential of the industry which may take the total premium of the industry to 3.8% of the GDP by FY26.

The Offer

65 is the retirement age for most people, but LIC wanted to shake the entire country’s financial system by launching an IPO worth ₹60,000 crore. In view of the market volatility arising as a result of the Russia-Ukraine conflict, it has reduced the IPO size and is now offering to open up a meagre 3.5% of the behemoth to public investors. The issue size now stands at ₹21 thousand crores.

IPO Details

| IPO Dates | 4th – 9th May | Listing on | BSE and NSE |

| Lot Size | 15 | Total Issue Size | up to ₹21,008 crores |

| Price Band | ₹902- 949 | Offer for sale: | up to ₹21,008 crores |

| Min investment | ₹14,235 | ||

| Basis of Allotment Date | 12-May- 2022 | Initiation of Refunds | 13-May-2022 |

| The credit of Shares to Demat Account | 16-May-2022 | IPO Listing Date | 17-May-2022 |

| Book running lead managers | Axis Capital, BofA Securities India, Citigroup Global, Goldman Sachs (India), ICICI Securities, J.P. Morgan India, JM Financial Consultants, Kotak Mahindra, Nomura Financial, SBI Capital Markets | Promoters: | The President of India, acting through the Ministry of Finance, Government of India is the company promoter. |

A special discount of ₹45 is being offered to retail investors and employees of LIC applying for the IPO. Meanwhile, a discount of ₹60 per share is being offered to the company’s policyholders.

LIC Financials

Let us look at LIC’s performance over the years

- LIC’s GWP(Gross Written Premium) and NBP (New Business Premium) on a consolidated basis increased at a CAGR of 9.21% and 13.49% from FY 19 to FY 21.

- The net premium and total income have been steadily increasing at 9.2% and 11.03% CAGR respectively.

- The expense ratio which is the cost incurred to manage the funds as a percentage of total funds has stayed in the range of 14-15%. This is lower than that of the top 5 private players.

- As of Dec’21, the company’s operating expenses as a % of total premium was 9.6%, which is lower than the top 5 private player’s OpEx of 12.1%.

- LIC’s Profit after Tax increased at a CAGR of 6.39% from FY 19 to FY 21.

- Notice the solvency ratio is consistently more than 1.5? It means that throughout this time, the company owns 1.5 times more assets than its debt.

Great, But What’s the Catch?

Under the IRDAI Investment Regulations, LIC is required to invest its assets in certain categories, subject to thresholds for investment. Due to this, LIC may be unable to manage market risks in the same manner as non-insurance companies.

Events such as changes in regulatory policies, volatility in capital markets, loss of customer confidence in the insurance industry or the company, sharp declines in its customers’ financial positions due to deterioration in economic conditions like the COVID-19 pandemic, etc. may cause discontinuations of insurance policies.

Arihant’s Outlook

The company’s long-term performance seems promising. Growing urbanization, the need for penetration, and LIC’s 65-year-old legacy, position LIC as a strong contender to grab the growth opportunity in this sector.LIC’s embedded value (EV) stood at ₹539,686 cr (as of September 2021). Based on its Sep’21 EV, IPO has been valued at 1.1x its EV which seems to be cheaper compared to other large private life insurer players.

{kind=link}