Utkarsh Small Finance Bank IPO is live. Should you Invest?

Utkarsh Small Finance Bank IPO is live. Should you Invest? Find out here.

In this article

- IPO details

- Issue details

- Offer Breakup

- IPO Strengths

- Key Risks

- Utkarsh Small Finance Bank Financials

📃About Utkarsh Small Finance Bank

The bank extends its facilities to individuals and businesses to assist them with their financial requirements.

The services offered by Utkarsh SFB include: Accounts and Deposits, Cards, Insurance and Investments, Loans

Ways to Bank

Customers of Utkarsh Small Finance Bank Limited can avail of features like a Top-up/Balance Transfer facility, Hassle-free processing with Easy Documentation Process, Avail loans up to Rs. 50 crores and Tenure up to 30 years, and efficient eligibility for salaried and self-employed individuals.

The company has a diverse product portfolio and microfinance remain a focused business segment.

The asset products of the entity include

Micro Banking Loans – Joint liability group loans and individual loans

Retail Loans – Unsecured loans, and secured loans

Wholesale Lending – Short-term and Long-term loan

housing loans with a focus on affordable housing, commercial vehicle/construction equipment loans, Gold loans

💰Issue Details of Utkarsh Small Finance Bank IPO

- IPO open from 12th July 2023 – 14th July 2023

- Face value: ₹10 per equity share

- Price band: ₹23 to ₹25 per share

- Market lot: 600 shares

- Minimum Investment: ₹15,000

- Listing on: BSE and NSE

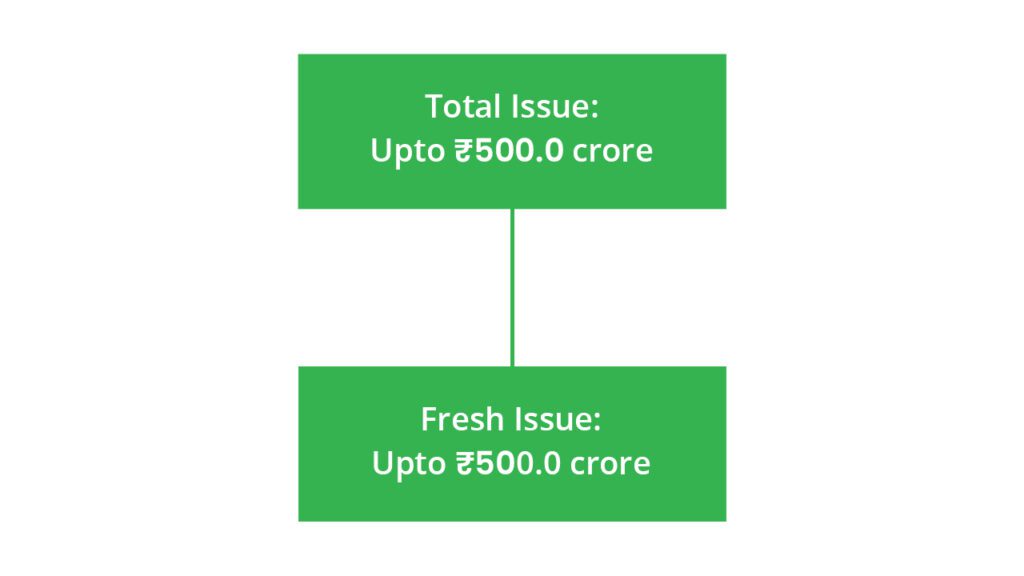

- Offer for sale: ₹500 Cr (Fresh Issue: ₹500Cr)

- Registrar: Kfin Technologies Limited

🪙Total Issue Price

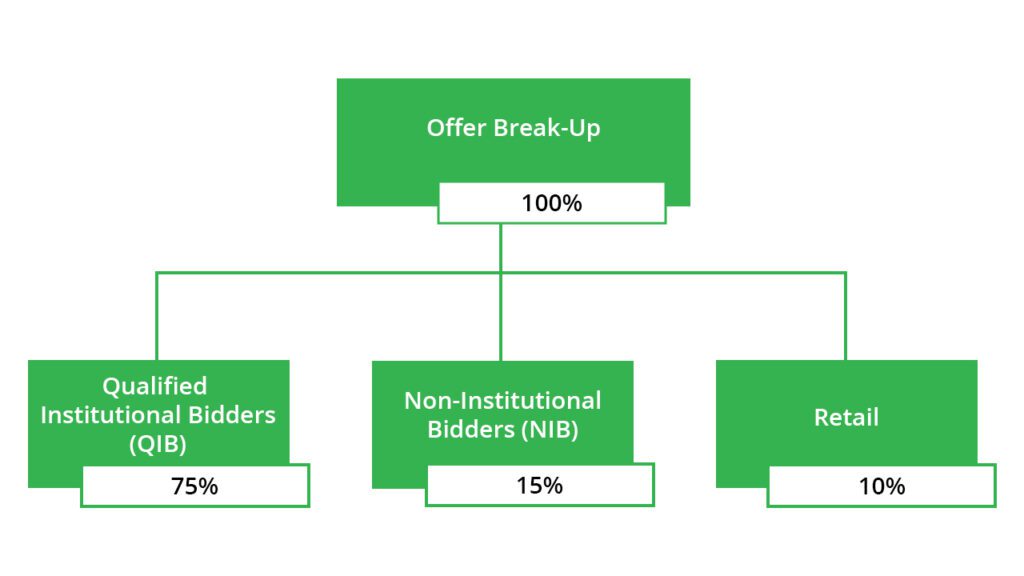

🪚Offer Breakup

🔭IPO Object

The Utkarsh Small Finance Bank Limited proposes to utilize the Net Proceeds from the Issue towards augmenting its Tier-1 capital base to meet its future capital requirements. Further, the proceeds from the Issue will also be used towards meeting the expenses in relation to the Issue.

⛓️IPO Strength

Some of the qualitative factors and strengths which form the basis for computing the offer price are:

- Diversified distribution network with significant cross-selling opportunities.

- Stable growth with cost-efficient operational performance

- They have a management team comprising qualified and experienced professionals.

- Sound understanding of microfinance segment and presence in rural and semi-urban areas.

- Focus on risk management and effective operations

🧨IPO Risk

- Their Bank’s business is vulnerable to interest rate risk, and any volatility in interest rates or inability to manage interest rate risk could adversely affect their Net Interest Margins, income from treasury operations, business, financial condition, results of operations and cash flows.

- Their Bank is subject to stringent regulatory requirements and prudential norms of RBI and any inability to comply with such laws, regulations and norms may have an adverse effect on business, results of operations, financial condition and cash flows.

- Their operations involve handling significant amounts of cash, making us susceptible to operational risks, including fraud, petty theft and embezzlement, which could harm their results of operations and financial position.

- They are dependent on their Key Managerial Personnel, and the loss of, or inability to attract or retain, such persons could adversely affect their business, financial condition, results of operations and cash flows.

💸Financial Data

| Period Ended | Total Assets | Total Revenue | Profit After Tax |

| 31-Mar-21 | ₹12,137.91 | ₹1,705.84 | ₹111.82 |

| 31-Mar-22 | ₹15,063.77 | ₹2,033.65 | ₹61.46 |

| 31-Mar-23 | ₹19,117.54 | ₹2,804.29 | ₹404.50 |

📬Also Read: Sustainable Investing in India: ESG Investments

{kind=link}